The last 12 months have been pivotal for the content industry. As the traditional boundaries of movie and TV licensing blur, studios and platforms are rethinking how audiences access content, balancing exclusivity with broader reach.

Looking ahead to 2025, the media industry will continue to shift toward greater flexibility in content distribution. Three significant trends are poised to shape the entertainment landscape: (1) the rise of co-exclusive licensing deals, (2) an increase in high-profile second-window sales, and (3) a resurgence of broadcasters as competitive forces in the acquisition market.

Movie licensing windows will become more fluid in 2025

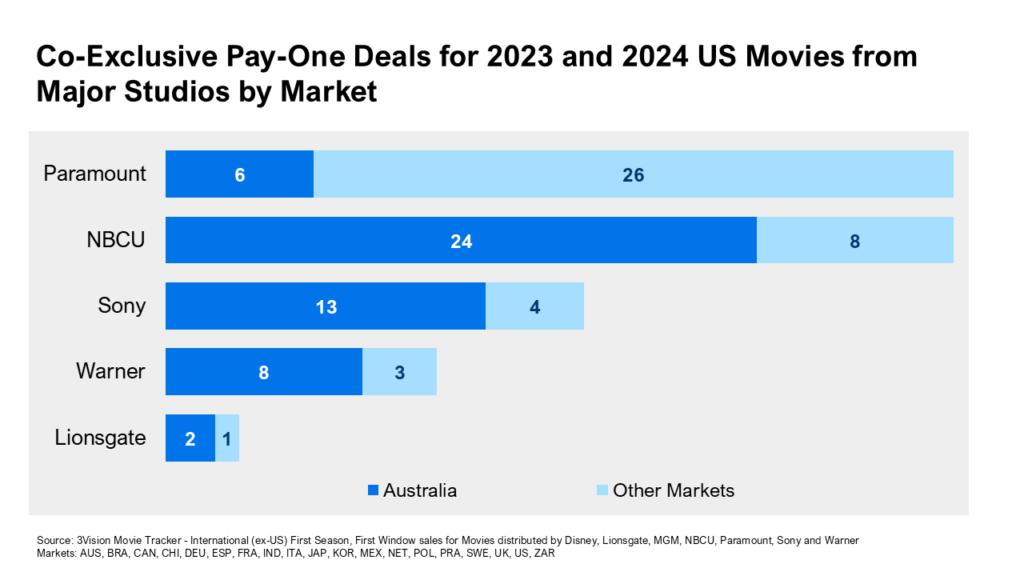

The movie licensing market remains an extremely valuable part of a title’s lifecycle. Many studios are now open to selling movies to multiple buyers simultaneously, creating co-exclusive deals for the pay-one window.

Australia is one of the largest markets for this activity, with pay TV operator Foxtel often sharing the pay-one window for high-profile studio titles with Netflix and Amazon.

Outside Australia, studios like Paramount have used co-exclusivity to maintain relationships with longstanding buyers – such as Sky in the UK, Germany, and Italy – while also supporting Paramount+ in those regions. Paramount has also shared pay-one windows with MGM+ in the US and Disney+ in Latin America.

Other buyers, such as Multichoice in South Africa and Wowow in Japan, have also shown willingness to share the pay-one window with SVODs like Netflix and Amazon.

While co-exclusive agreements are less common for scripted TV than for film, there have been some notable examples, such as Disney licensing Reservation Dogs to both Crave and CBC in a second window in early 2024. More common in TV is the practice of licensing titles that debuted on Disney+ internationally in the first window, without removing them from Disney+ for second-window buyers.

These co-exclusive deals have long been a staple for the likes of Foxtel. Many other buyers have become similarly open to sharing with studio D2C services if it means making major movies available to their viewers. As this is the only avenue to acquiring high-profile titles in a timely manner, we can expect to see the trend continue into 2025.

Studios will license more high-profile titles to third parties

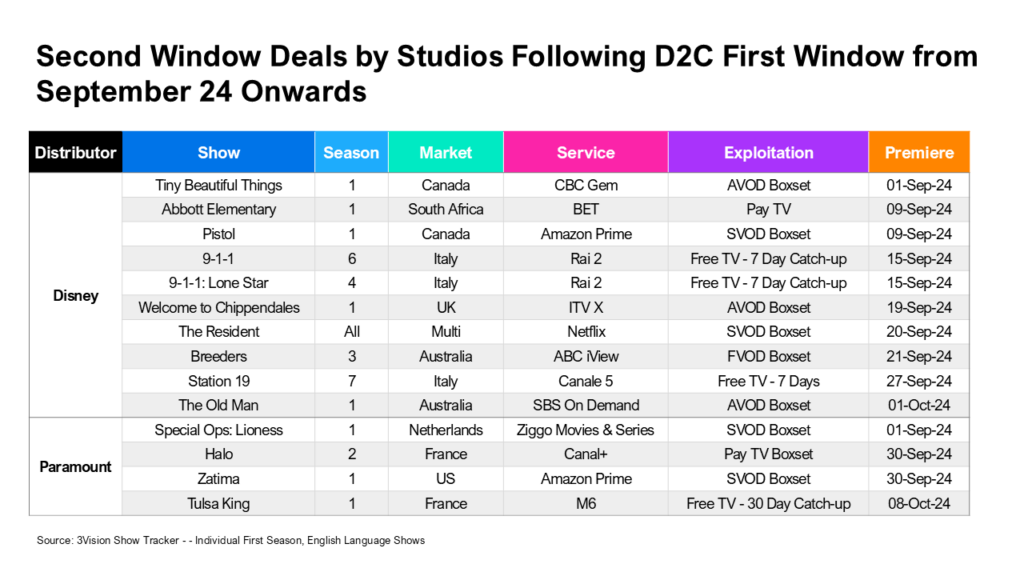

Co-exclusivity is only part of the story. 2024 saw studios, particularly Disney and Paramount, significantly increase second-window sales to third parties after titles debuted on their own D2C services.

Disney has focused heavily on the free TV audience, both for linear channels and free TV-owned digital platforms. Repeat customers include ITV and BBC in the UK, SBS in Australia, and CBC in Canada.

Historically, buyers have been a little wary of acquiring titles in a second window after SVOD; often, they could not be granted rights that allowed them to simultaneously release all episodes on their service (known as “boxsetting”). In 2024, however, boxsetting became quite common for these types of acquisitions, with the caveat that titles will still be available on their original service.

For the likes of Disney, this can result in a win-win situation. Disney licensed the first season of Extraordinary to ITVX a month ahead of its second season debuting on Disney+. These innovative deals not only allow studios to gain additional revenue without giving up a title’s place on its SVOD service but also to use the sale to drive awareness and excitement for new seasons.

In 2025, interest in second-window deals will continue to rise among broadcasters fighting back against a streaming-dominated landscape.

Broadcasters will crack the garden wall

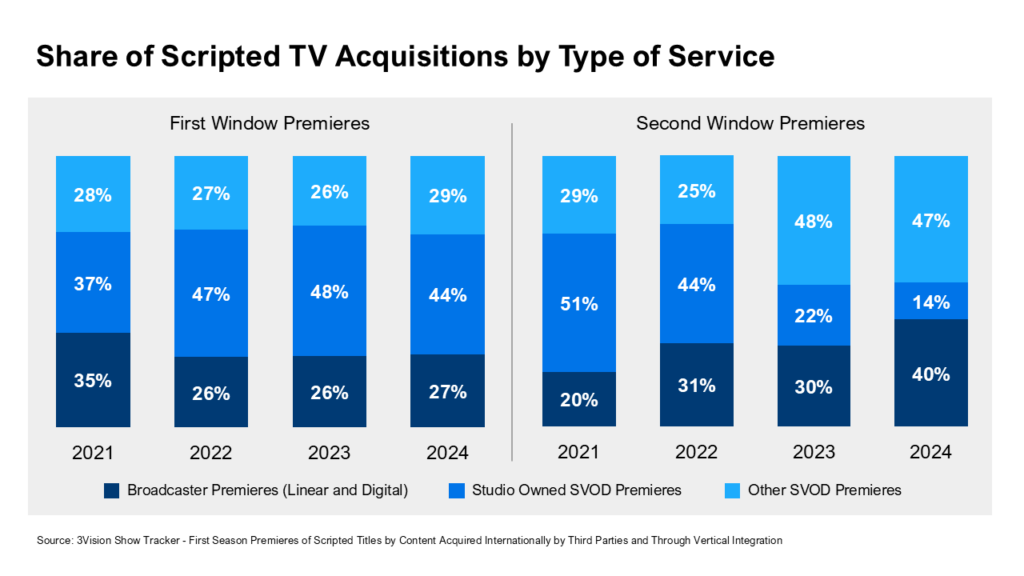

The rollout of SVOD services initially marginalized broadcasters in the acquisition market, as studios prioritized folding their titles into studio-owned platforms like Disney+, Paramount+, and Max. This shift limited broadcasters’ access to both first-window and second-window content, reinforcing studio-owned “walled gardens.”

But cracks in the walls are starting to appear. Broadcasters have grown to form a sizeable chunk of the second-window acquisition market in several territories. Meanwhile, marginal growth by broadcast companies in the first window – and a slight reduction in studio acquisitions – signals that broadcasters may yet have opportunities to boost their activity in 2025.

Coupled with broadcasters more frequently securing enhanced catch-up rights for their acquisitions, the trend has allowed broadcasters to slowly foster AVOD platforms of their own.

Supported by both linear and VOD-only content acquired exclusively for their digital companion services, broadcasters will continue to push back for greater market share in the year ahead.

Looking ahead at the streaming industry in 2025

In 2024, the distribution market was largely defined by studios opening their walled gardens, driving many other phenomena that extend into 2025.

In movie distribution, the destruction of the status quo by COVID and the ongoing launch of studio-owned SVODs around the world continue; co-exclusivity, it seems, is here to stay.

Studios’ newfound willingness to sell to third parties in the second window has allowed broadcasters to re-enter the second-window market for high-profile series. Re-establishing these distribution relationships will inevitably enable broadcasters to claw back at least some share of the acquisitions they lost during the initial years following the launch of studio-owned SVODs.

The media industry’s move towards more flexible and collaborative distribution strategies opens new avenues for revenue and allows for greater audience engagement across diverse platforms. For studios, balancing exclusivity with strategic partnerships will be key to maximizing content reach and profitability; broadcasters have an opportunity to regain strength in a market that has rapidly shifted toward digital consumption. By staying agile and embracing these changes, media businesses can thrive.