The growth of AI and ML in business

Artificial Intelligence (AI) and Machine Learning (ML) have been at the innovation forefront across many industries, solving problems as varied as facial recognition, self-driving cars, and even recommending a nice movie to watch with the kids.

According to a McKinsey report on AI adoption, nearly 50 percent of respondents report that their companies have adopted AI in at least one business function, with a small contingent of respondents claiming that 20 percent or more of their earnings are attributable to AI.

Rising costs associated with greater transactional volumes, more diverse payment avenues, and rising Financial Intelligence Unit (FIU) costs have led many large financial institutions to incorporate AI and machine learning to alleviate alert volumes while ensuring increased risk coverage.

The large-scale adoption of AI across various industries begs the question: How has AI translated into AML and BSA functions at banks?

With increasing financial crime compliance, we were curious to understand whether the industry has adopted the efficiencies and innovations of AI and machine learning. As a result, SymphonyAI, in association with ACFCS, conducted an international survey to understand the state of AI adoption in AML.

The survey, sent to a curated list of ACFCS members, focused on:

- Understanding the current state of AI adoption in AML programs

- Types of AI/ML currently in use

- AI implementation by region, size of bank, and function

Barriers to more wide-scale AI from a regulatory perspective

Regulators encourage machine learning

US and European regulators have signaled their interest in banks leveraging machine learning as part of their risk management framework.

In the United States:

Pilot programs undertaken by banks, in conjunction with existing BSA/AML processes, are an important means of testing and validating the effectiveness of innovative approaches. While the agencies may provide feedback, pilot programs in and of themselves should not subject banks to supervisory criticism even if the pilot programs ultimately prove unsuccessful. Likewise, pilot programs that expose gaps in a BSA/AML compliance program will not necessarily result in supervisory action with respect to that program.

– Joint statement by FinCEN, FDIC, OCC and the Board of Governors of the Federal Reserve

This stated encouragement for compliance programs to include “innovative technologies,” along with the acknowledgment that pilot programs should not subject banks to increased supervisory criticism, is a strong indicator of regulator focus on new technologies such as AI and machine learning to aid in AML/CTF detection.

Also significant is US regulatory support of AI and ML in the Anti-Money Laundering Act of 2020, which encourages “innovative approaches such as machine learning or other enhanced data analytics processes” to reinforce financial institutions’ and FinCEN’s crime detection capabilities.

In Europe:

The Financial Action Task Force (FATF) has recommended utilizing a risk-based approach to AML and has been outwardly open to AI adoption. They’ve stated that advances in machine learning and AI “provide opportunities for supervisors to glean additional useful supervisory insights and identify risk trends across sectors and groups of regulated entities.”

So, current regulatory guidance definitely encourages the testing and adoption of machine learning to augment rule-only monitoring of transactions.

Data overload requires next-generation tech

Compliance leaders have been questioning the efficacy of rule-based detections and have begun experimenting with next-generation technologies to augment existing legacy technologies.”

From a recent study by Aite-Novarica Group

In developing this survey, we reviewed the current challenges and the advancements already made in AI/ML adoption. We proceeded with several assumptions based on our depth of experience:

- Legacy monitoring solutions produce a high volume of false positives. More importantly, they may not adequately cover all risks.

- Advancements in computing power, automation and analytics have enabled better handling of AML operational challenges.

- Regulatory pressure, banks dealing with long implementation times, ineffective risk controls and increasing operational costs have led to greater adoption of machine learning and automation technologies to reduce cost and increase efficiency.

- The volume and depth of data have been exploding over the past year. According

to an IBM study, it is estimated that we produce 2.5 quintillion bytes of data

every day…and 90 percent of the world’s data has been produced within the last two years.

With banks sitting on significant volumes of data on customer behaviors, interactions and profiles, leveraging this data requires stronger processing, next-generation technologies and data science expertise.

Survey design and population

Sent to a curated list of ACFCS members, the survey focused on the current state of AI adoption in AML programs, types of AI currently in use and barriers to adoption. Respondents were banking professionals within Compliance and AML.

Participants represent a variety of institutions, primarily across the US and Europe.

- 49% work for banks with less than $10 billion in Assets Under Management (AUM)

- 30% work for larger institutions with more than $50 billion AUM (chart #1)

- 30% work in community banking

- 25% work in retail banking

Regulatory evolution impacts AI adoption

Almost half of the survey participants believe that recently enacted legislation, such as AMLA 2020 in the US and the 6th AML Directive in Europe (including UK), will impact their bank’s adoption of AI and machine learning (chart #3).

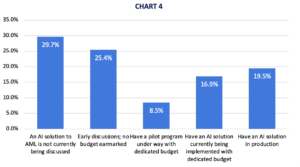

- 47% tell us their bank has some sort of budget set aside for AI projects, either for pilot programs or full-scale production implementation (see chart #4).

The survey also revealed that AI adoption varies by asset size of banks. Smaller banks do not yet employ machine learning. However, among larger banks:

- 62% of banks with $21B or more in assets have some form of AI adoption.

- About a third of banks with less than

21B in assets have adopted AI.

Among the types of AI and machine-learning technologies employed, the most popular is the traditional rule-based detection framework.

- 93% use automated rules within their BSA/AML compliance programs

- 37% use predictive models

- Fewer use more advanced technologies like network analysis and text mining

(26% each)

While only 22% of banks with less than $10B AUM leverage predictive models, more than half of the banks with greater than $50B AUM are doing so.

Analytics can boost AML capabilities

We know from experience that analytics greatly improve AML proficiency.

Our survey shows a high rate of analytic adoption in TMS and alert, triage, and investigative operations, but not in KYC and customer segmentation.

While banks appear eager to use analytic techniques in production for Data Collection and Customer Risk Scoring, they’ve not yet widely adopted such techniques in KYC/CDD and Risk Identification and Scenario Development.

Our recommendation is simple: Let your analytics do their job by highlighting your business processes that need improvement.

The chart below identifies specific areas in which analytics can be used to improve intelligent decision-making, effectively simplifying and optimizing daily activity.

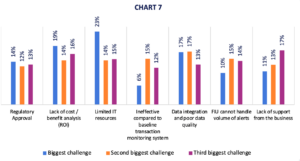

Top challenges to AI adoption

The top three challenges identified by our survey respondents, regardless of size, are:

1. Lack of IT resources

Our response:

Newer cloud-based technologies enable shorter implementation times – typically under 6 months – and often provide proof of value results in as few as 6 weeks, significantly reducing strain on IT departments.

2. Data integration and poor data quality

Our response:

Data quality doesn’t have to impede implementation of systems designed to provide greater operational efficiency, lower Total Cost of Ownership (TCO) and stronger risk coverage. Our AI-based, AML systems incorporate dynamic data models that leverage the same data being fed into existing Transaction Monitoring Systems and increase the informational yield from existing data.

3. Lack of support from the business

Our response:

A business case can be made with a Proof of Value (POV) project…a time-limited program that demonstrates the advantages of the newer technology with limited bank employee engagement and definitive results. POV projects range from 6 to 10 weeks and enable a business team to build a strong case to overcome most objections.

Case study: Tier-1 bank knew its legacy TMS was overlooking risk

The situation

A Tier-1 commercial, retail, corporate, and correspondent bank was facing significant pressure to meet regulatory SLAs for investigatory burndown. They were experiencing year-over-year alert growth, with relatively few alerts leading to SAR filings.

The goal

As their stated corporate priority was to expand on data-driven capabilities to make intelligent decisions regarding the prevention and detection of financial crimes, it was imperative for them to identify risk that their legacy TMS was missing.

The process

The client provided anonymized data covering almost two years of transactions, accounts, and customers for one business line. With the data being an exact replica of TMS input data, deployment was reduced to hours instead of months.

The results

Using the same data as the client’s legacy TMS, Sensa uncovered a wealth of new, high-risk events and previously unknown or hidden customers. The following results were delivered:

In summary, this survey reveals

- Legacy technologies for detecting financial crime are becoming obsolete at neck-breaking speeds

- Machine learning and AI are steadily picking up the slack of obsolete systems

- More banks are dedicating budgets and resources to combat the inadequacies of legacy technologies

- This adoption is being ushered in by changes in the regulatory viewpoint, with regulators recommending a risk-based approach to AML

- As AI gains traction, case studies show the efficacy of implementing true AI in risk detection

Increase risk detection and alert quality in just four months

It’s more critical than ever for FIs to team up with technological experts who can apply AI to deliver holistic visibility into the discovery of financial crime and fraudulent behaviors.

At SymphonyAI, we’ve proven our expertise time and time again.

Our solutions transform how financial crime is detected, liquidity and risk are managed, and how intelligence is gathered. And it doesn’t take long to prove our value. In fact, SymphonyAI delivers on our promises in just four months from project implementation. Let us show you how.